Les actualités de la BRVM en Flux RSS

Les actualités de la BRVM en Flux RSS

Nous agrégeons les sources d’informations financières spécifiques Régionales et Internationales. Info Générale, Economique, Marchés Forex-Comodities- Actions-Obligataires-Taux, Vieille règlementaire etc.

Enjoy a simplified experience

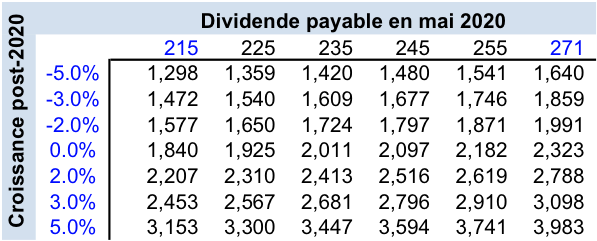

Find all the economic and financial information on our Orishas Direct application to download on Play StoreSummary : We estimate that the stock is worth FCFA 2.207, or about 5% more than the current price of FCFA 2.100. Our analysis is based on a dividend per share of FCFA 215 payable in May 2020 (figure not validated by BOAM, lower limit of our dividend range per share of FCFA 215 to 271 for 2020) and a yield requirement of 12 % per year. More frequent and more exhaustive financial communications from management would make it possible to refine the range and revise our estimate of the cost of capital (12%).  The last price as well as the min and max prices for the last 12 months are in CFA Francs (FCFA) per share . Sources: Capital IQ, BRVM website consulted on 30/8/2019 .

The last price as well as the min and max prices for the last 12 months are in CFA Francs (FCFA) per share . Sources: Capital IQ, BRVM website consulted on 30/8/2019 .

Founded in 1982 in Bamako, Bank of Africa – Mali (BOAM) is one of the oldest banks in Mali serving both corporate, SME and individual customers. At the end of 2018, the bank's capital was divided into 15.45 million shares held at 61.4% by BOA West Africa, a subsidiary of the Moroccan banking group BMCE Bank of Africa, alongside private shareholders (36.5%) and 'Attica SA (2.1%), a Greek holding company operating mainly in maritime transport.

At the end of May 2016, BOAM was admitted to the BRVM with a free float of 21.4% representing 3,313,410 shares. Between its IPO and the close of trading on 08/29/2019, BOAM shares lost nearly 75% of their value.

We arrive at this figure of 75% by comparing the price of FCFA 2,100 on 08/29/2019 with the volume-weighted average price of the first month of listing (May 31, 2016 to June 30, 2016) which amounts to FCFA 8,307 after taking into account the split of December 21, 2017.

Despite this stock market debacle, is the title a good investment at the price of FCFA 2,100? Let's analyze it all!

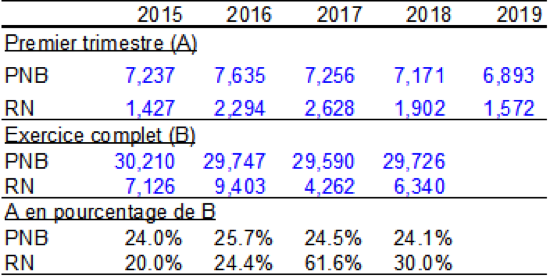

Unlike its main competitors, the bank has struggled to grow since 2015 with net banking income (NBI), the main measure of a bank's volume of activity, which has stagnated around XOF 30 billion (see table B) while its counterparts BNDA and BDM saw their business volumes increase over the same period. While BOAM's GNP fell by 0.5% per year between 2015 and 2018, that of BNDA experienced an annual increase of 7.1% over the same period to stand at FCFA 36.4 billion for the 2018 financial year. Between 2015 and 2017, the last year for which we have audited figures for the institution, BDM's GNP grew by 8.7% per year to stand at FCFA 34.6 billion.

TECHNICAL POINT 1

We could have a debate on the relevance of BNDA and BDM as comparables for BOAM but any critic in good faith will recognize that the three banks, historical players in the Malian banking landscape, are of similar sizes (GNP of FCFA 30 to 36 billion) , and are subject to the same competitive pressures as well as the same macroeconomic, political and security risks.

The results for the first quarter of 2019 echo the disappointing performance of previous years with a contraction in quarterly NBI of 3.9% or 278 million compared to the same period last year. The net result also contracted by more than 17.4% or FCFA 330 million. It should also be noted that the NBI for the first quarter fell below the symbolic bar of FCFA 7 billion for the first time in 4 years , a sign that the bank is in decline in an increasingly competitive environment also marked by uncertainty as to developments in the security and political situation in Mali. As for the net result (NR) for the quarter, it is also at its lowest for 4 years and stands at around FCFA 1.5 billion.

Table A – NBI and NR of the first quarter (figures in FCFA millions)

Sources: Quarterly and annual reports published by BOAM and consulted on the BRVM website .

What to expect for the rest of the year?

The table below summarizes the contribution of the first quarter results to the annual performance between 2015 and 2018. This analysis will allow us to form an opinion on the bank's outlook for the rest of 2019.

Table B – First quarter results and annual results between 2015 and 2018 (figures in FCFA million)

Sources: Quarterly and annual reports published by BOAM and consulted on the BRVM website .

Based on these data, we anticipate for 2019 a NBI in the range of FCFA 28.0 to 28.6 billion and a net profit in the range of FCFA 5.0 to 6.3 billion . The lower limit of our range was obtained by extrapolating to the rest of the 2019 financial year the decreases (in value) in NBI and net income observed in the first quarter to the rest of the year 2019 (Table C).

Table C – Calculation of the lower limit of the 2019 projections (figures in FCFA millions)

Sources: Quarterly and annual reports published by BOAM and consulted on the BRVM website, author's calculations

The upper limit of the range was obtained by treating the NBI and the result of the first quarter as respective contributions of 24.6% and 24.8% to the annual results, in line with the average between 2015 and 2018 (excluding 2017 due to the very recorded – for bad debts – during this financial year). See Table D.

Table D – Calculation of the upper limit of the 2019 projections (figures in FCFA millions) .

Sources: Quarterly and annual reports published by BOAM and consulted on the BRVM website, author's calculations

TECHNICAL POINT 2

There are other methods than those presented in tables C and D for projecting the annual results of a company, but in the absence of indications from management and the availability of a consensus of analysts, we have no other choice than to make approximations based on reasonable assumptions.

Based on our projections (not validated by BOAM management) and a distribution rate (the share of profit that is paid to shareholders in the form of a dividend) in line with 2018 (71%), we anticipate a dividend per share in the range of FCFA 215 to FCFA 271 after taking into account the tax on income from securities (IRVM) at the rate of 7%.

How do you know what the fair price to pay for the stock would be based on the expected dividend?

To be conservative, we will take the lower limit of our estimate of the 2019 dividend (FCFA 215 per share payable at the end of May 2020) as the basis for valuing the BOAM share . After 2020, we anticipate, again to be conservative, that dividend growth will be limited to 2% per year, slightly more than the inflation rate observed in Mali in 2018 (1.7%).

That is, after 2019, we expect the bank's profit to grow only 2% per year, and the payout ratio will remain unchanged at 71%. We will also retain a discount rate of 12% as the required return (i.e. approximately twice the after-tax return on 7-year Malian government bonds. See for example the issue of 04/02/2018 at the rate of 6.50% with maturity in 2025 ).

We are aware that the 15% rate of return is high, but given the difficult political and macroeconomic context in which BOAM operates and the low level of information we have on the company's results and outlook (quarterly reports of a single page, no quarterly information session open to all shareholders), we must demand a return that remunerates us sufficiently for the risk we accept to take. With more transparency (e.g. a more detailed quarterly report and a six-monthly Q&A session with management) and representation of small shareholders on the board of directors, we could revise our yield position down to require to agree to hold BOAM shares.

TECHNICAL POINT 3

Some financial theorists and practitioners will tell you that the required rate of return should only compensate for systemic risks, ie those that affect all companies at the same time, such as economic or political crises. According to them, the specific risks of a company must be managed by investors through diversification, i.e. buying shares of a large number of companies and investing in other classes of companies. assets (treasury bills, bonds, real estate, works of art, precious metals, venture capital). We are of the opinion that this approach does not apply to small holders who would consider an investment in BOAM because they very probably have access to few investment opportunities apart from securities listed on the BRVM. The good lady who entrusts her money to the managers and boards of directors of companies listed on the BRVM does so with in mind the project of having a home, sending her children to a good university or having a net of security for his old age. She deserves that her hard-earned money be remunerated at its fair value and, at the very least, that her capital be preserved. This is our opinion, other investors might settle for 8% or 10% return because they only want to be compensated for systemic risks. Others will ask for 20% or more for their own reasons.

By using the dividend discount mod el (DDM ie discounting future dividends) valuation method, our assumptions lead us to a share value of FCFA 2.207 per share, i.e. 5% more than the price on 08/29/2019. Therefore, we consider the stock to be a good investment opportunity. Not a great deal, but a good deal anyway . The table below shows the stock valuation for different dividend and dividend growth assumptions.

Table E – Stock Value for Different Dividend and Growth Assumptions .

12% return requirement (figures in FCFA per share)

Commentary on Table E

Each value in the table corresponds to the maximum price that the investor should be willing to pay who anticipates a certain level of dividend per share for 2020 and a certain level of growth in the dividend per share after 2020.

For example, the figure of 3.153 at the very bottom left of the table means that the investor who expects a dividend of FCFA 215 per share and an annual dividend increase of 5% after 2020 should be ready to pay up to at FCFA 3.153 per share if like us it has a 12% return requirement. This would mean that from this investor's point of view, the BOAM stock is currently undervalued and presents an opportunity to make a gain of 50% or FCFA 1,053 by buying the stock at the current price of FCFA 2,100.

>

>

Vous devez être membre pour ajouter un commentaire.

Vous êtes déjà membre ?

Connectez-vous

Pas encore membre ?

Devenez membre gratuitement

20/07/2026 - Economie/Forex

20/07/2026 - Economie/Forex

17/07/2026 - Economie/Forex

15/07/2026 - Economie/Forex

13/07/2026 - Economie/Forex

13/07/2026 - Economie/Forex

10/07/2026 - Economie/Forex

09/07/2026 - Economie/Forex

09/07/2026 - Economie/Forex

20/07/2026 - Economie/Forex

20/07/2026 - Economie/Forex

17/07/2026 - Economie/Forex

![[Stock Market Opinion] Bank of Africa Mali (BOAM), a good investment opportunity?](/uploads/news/BOAMali.jpg)